what is a Tax System and Why Does It Exist?

Governments collect revenue through a tax system. Tax revenue supports the important needs of our society such as: education, healthcare, transportation, and public safety.

It is impossible for governments to provide any of these critical services without generating revenue through taxation.

As an example, when you pay your property taxes, those funds go toward helping your local school district provide teachers and maintain the school’s facility.

When you shop and pay sales tax, a portion of that sales tax goes to your state government to help maintain highways and bridges.

It is the collective obligation of each member of society to help support the operation of the community. It is regardless of whether a person is supporting the community by paying their income taxes or through purchasing items and paying sales tax.

Let’s dive through this complete guide to taxes for beginners and experts.

Economic Purpose of Taxes

Taxes provide funding and support the economy and society. So, we can say that it is vital to know tax basics for beginners and experts both

The government uses taxes in the following manner:

- The use of progressive taxes ensures that those who earn a higher income pay a larger tax.

- Controlling inflation by changing the amount of money available for citizens to spend by changing the tax rate.

- Encouraging investment by providing tax deductions for retirement accounts or educational expenses.

- Fostering the implementation of certain behaviours or activities, such as implementing renewable sources of energy.

In practical terms, a family who installs solar panels can receive a 30% tax credit for installation costs. This financial incentive will encourage families to adopt renewable sources of energy, also reduce their tax obligations.

Direct vs. Indirect Taxes

In the United States, taxes can be classified into two groups:

1) Direct taxes are paid to the government based on profits or income.

The federal government’s income tax, state income tax, and income tax on wages are all examples of this type of tax.

The amount of direct tax is defined by how much money the tax payer has available to be taxed.

2) Indirect taxes are paid on the purchase of goods and/or services. An example of an indirect tax is a purchase sales tax on an item you have purchased.

Indirect taxes are transferred from the seller to the buyer. Therefore, it has no direct relationship to the buyer’s income.

Once a taxpayer understands the difference between direct and indirect taxes, they can more easily identify how they are contributing to the tax system.

How Taxes Work in the USA?

Federal vs. State vs. Local taxes

In the United States, there are three different types of taxes such as federal taxes, state taxes, and local taxes. Each tax level has its own rules, and the rules for each level don’t necessarily match.

| Tax Level | Description | Real Example |

| Federal | Nationwide taxes collected by the IRS | Federal Income Tax on wages |

| State | Taxes vary by state | State Income Tax in California (9.3% for $61k–$312k income) |

| Local | City or county-level taxes | Property tax in New York City for homeowners |

An individual residing in Texas may not remit any state income taxes.

However, this person will be required to remit federal taxes and will also pay property tax or sales tax. This shows how your geographical location can impact how much tax you need to pay to the government.

Role of the IRS

The IRS is responsible for collecting federal taxes for the United States and has many key responsibilities, such as:

- Processing of tax returns

- Issuing refunds to taxpayers

- Conducting audits of taxpayers to adhere to tax laws

- Providing helpful guidance regarding tax laws to taxpayers.

For example, if you are not sure how to report income earned from being a freelancer, the IRS offers different forms to report earnings from freelancing.

Overview of Tax Flow

The process of how taxes flow through our economy and how they are paid is cyclical and impacts every taxpayer in the United States:

- Earning income: Your wages, independent contractor income, or profits earned from running a business.

- Tax Withholding or estimating tax payments: Employers withhold taxes for federal and state purposes from your paycheck. Independent contractors estimate their tax liability four times a year and remit payment.

- Calculating tax liability: Using your total taxable income and subtracting any deductibles or credits available to you at the end of the year.

- Filing your tax return: You will submit your income, deductibles, and any amount of tax you owe.

- Receiving a refund or paying taxes: Depending on how much tax was withheld or estimated, you will either be entitled to receive a tax refund or owe more taxes.

This cycle continues each year and ensures that every taxpayer contributes to the cost of running the government fairly.

Complete Tax Lifecycle

By gaining knowledge of all aspects relevant to your tax life, you can minimize errors while perfectly planning for your taxes.

Earning income

Sources of income include:

- Earned wages through an employer

- Gained cash as an independent contract worker (freelance/gig economy)

- Profit made through the operation of a business

- Yield from the sale or investments of stocks/bonds/real estate

For example, if Jane earned a total of $50,000 through her employer and $10,000 as a freelance writer, Jane must report both amounts to the federal government for purposes of determining her tax obligations.

Recording and reporting income

It is extremely important to maintain an accurate record of your earnings.

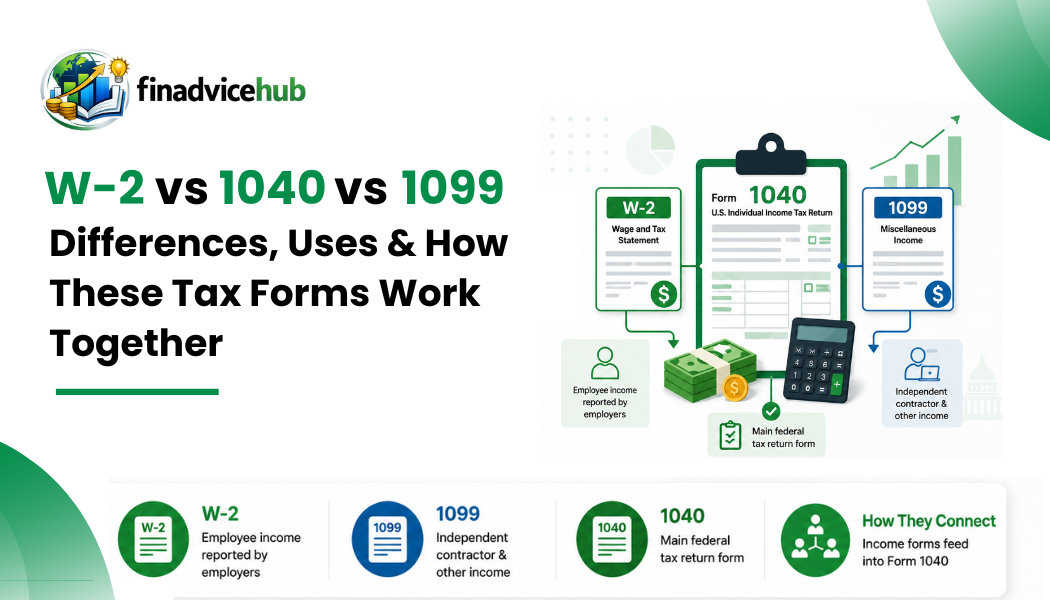

- You will receive a W-2 from your employer

- Freelancers receive 1099s from independent contractors

- Business owners must keep complete accounting records

If any part of your income is not reported accurately, it may result in an audit, fine or interest against you by the IRS.

Calculating tax liability

To figure out the tax you owe, you have to look at:

- Your total income

- Your adjustments (for example, contributions to retirement)

- Your deductions (for example, mortgage interest)

- Your credits (for example, Child Tax Credit)

Example: John’s total earnings are $80,000 in salary and $5,000 in dividends. If John qualifies for deductions and credits, he may owe only $12,000 in taxes after those deductions and credits are considered.

Understanding Taxable Income

Gross Income vs. Taxable Income

- Gross Income = Total Income Before Any Deductions and Adjustments

- Taxable Income = Income IRS Taxes After Deductions and Adjustments

Example: Jane earns $80,000 in salary; however, she contributes $5,000 to a 401(k) retirement plan. Therefore, Jane’s taxable income will be only $75,000 instead of $80,000.

Adjusted Gross Income (AGI)

AGI is your income less certain adjustments (such as contributions to your 401(k) or Student Loan Interest) but prior to applying the standard deductions or itemized deductions.

AGI is used to decide whether you can claim certain credits and deductions.

Common AGI Adjustments:

- Student Loan Interest

- Health Savings Account Contributions

- Retirement Plan Contributions

Example: Sarah earned $100,000; made a $10,000 contribution to her IRA; and paid $2,000 in student loan interest. Sarah will have an AGI of $88,000.

Tax Brackets Explained (With Example)

The IRS uses a graduated rate tax schedule that places higher rates on higher levels of earnings.

However, this applies only to income that is within each corresponding tax bracket based on your filing status.

For any earnings that fall into a specific tax bracket, those earnings are taxed at the corresponding rate.

| Income Bracket | Tax Rate | Applied To |

| $0 – $11,000 | 10% | First $11,000 of taxable income |

| $11,001 – $44,725 | 12% | Next portion of income |

| $44,726 – $95,375 | 12% | Next portion of income |

How tax brackets work with example?

Step-by-step example:

Mike has $50,000 in taxable income:

$11,000 taxed at 10% ($1,100)

$33,725 taxed at 12% ($4,047)

$5,275 taxed at 22% ($1,160)

Total Federal Income Tax of $6,307.

There are many other misunderstandings, including:

- “I am taxed at the top of the bracket”

- “I will lose money due to moving into a higher bracket”

- “The only amount of income that you are taxed at a higher rate is income that falls within the brackets of that tax schedule.”

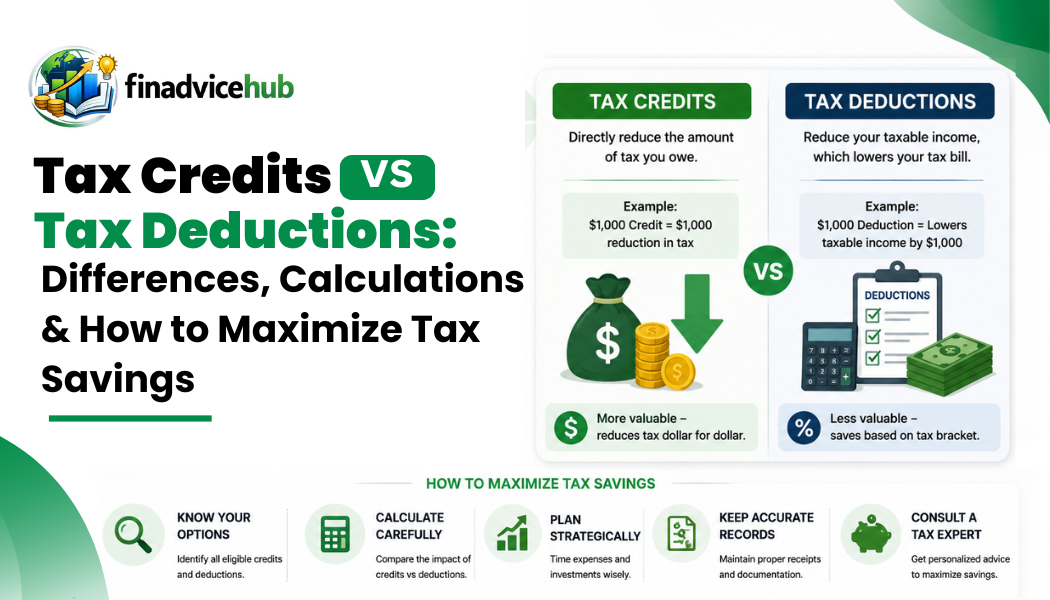

Tax Deductions vs. Tax Credits

Understanding the difference is important to plan for taxes in a smart way.

| Features | Deductions | Credits |

| Reduces | Taxable Income | Tax owed directly |

| Impact | Varies by tax bracket | Fixed, more impactful |

| Example | Mortgage interest | Child tax credit |

Practical tip: Credits typically have a bigger impact than deductions because they reduce your taxes dollar-for-dollar. Therefore, a child tax credit of $2000 will lower your tax liability by $2000.

Step-by-Step Tax Calculation Framework

Formula:

Gross Income – Adjustments = AGI – Deductions = Taxable Income × Tax Rates = Tax Liability – Credits = Final Tax

Tax Calculation Example USA – Salary Case:

John makes $70,000 gross income, has AGI of $65,000 after 401k contributions, takes the standard deduction of $13,850 and ends up with taxable income of $51,150.

His federal tax liability would be about $6,100, before considering any credits; he ended up with $5,000 after accounting for his credits.

Freelancer Example – how tax deductions work in real life?

Sarah generated $50,000 in revenue from self-employment activities.

In addition to being liable for self-employment taxes of approximately $7,650, she has also made estimated tax payments on a quarterly basis to reduce penalties for underpayment.

After deducting her expenses, Sarah’s taxable income is $40,000. It resulted in an estimated total federal income tax liability of approximately $5,200.

Tax Filing Process USA

Thinking about how to optimize tax filing? Completing tax returns can seem like a challenge, but if broken down into manageable parts, the process becomes much simpler.

Required Documents

- W-2 forms for employer-owned company income

- 1099 forms for independent contractor income

- Investment account statements for capital gains tax purposes

- Documentation to support any deductions (receipts, records)

Filing Status

Your filing status has an impact on your tax brackets and possible deductions.

Your filing status options include:

- Single

- Filing married jointly

- Filing married separately

- Head of household

Selecting an incorrect filing status may result in paying more taxes than needed.

Filing Methods

Use any of the following:

- Computer software (TurboTax, H&R Block, TaxSlayer)

- Licensed tax-preparers (such as a Certified Public Accountant (CPA) or a licensed enrolled agent)

- Mail-in income tax returns (not done as often today)

Example: An independent contractor (Sarah) may not want to file independently but to hire someone to assist with the calculation of quarterly estimated tax payments. She also needs someone to decide which calculators to use in calculating home office deductions.

Deadlines

- Federal taxes are due April 15

- Extensions: Form 4868 gives six months

- Late filing penalties begin immediately after the filing deadline.

After Filing

- Monitor your refund status online.

- Make sure that you have paid all of your tax liabilities.

- Maintain records for three to seven years in case of an audit.

Tax Optimization Strategies

The legal way to optimize your taxes can lead to a good source of savings.

Reducing taxable income

- Increase your contributions into qualified accounts such as 401(K), IRA, or HSA.

- Claim student loan interest deduction and/or the educational expense deduction.

Maximizing deductions

- Itemizing allows taxpayers to deduct expenses such as: mortgage interest, medical and charitable contributions for which receipts are retained

- Home office deduction for freelancers (self-employed)

Using credits effectively

- Child tax credit, education credits and home improvements that meet the energy efficient standard

Adjusting withholding

Employers can adjust their employee’s withholding allowances for taxes based upon projections regarding the actual amount that will be owed on his/her taxes.

Example Table – Optimization Strategies:

| Strategy | Who It Helps | Potential Savings |

| 401(K) Contribution | Salaried employees | $2,000–$5,000/year |

| Home Office Deduction | Freelancers | $500–$2,000/year |

| Education Credits | Students/Parents | $1,000–$2,500/year |

Common Tax Mistakes Beginners Make

Common blunders that can cost money, time and stress:

- Incorrect income being reported.

- Not claiming deductions/credits.

- Incorrect filing status.

- Late filing.

- Not paying Self Employment Tax or Quarterly Estimated Tax.

Example: Small business owner underestimated employment taxes owed $3,000 plus interest in penalties. Even if full payment cannot be made, timely filings lower penalty amounts.

What Happens If You Don’t File or Pay Taxes?

| Consequences | Explanations |

| Penalities | Up to 25% of unpaid taxes for late filing |

| Interest | Accrues daily on unpaid amounts |

| IRS Actions | Notices, wage garnishments, bank account seizures |

Even if you cannot pay the full amount, filing on time reduces penalties.

Real-Life Tax Scenarios

Salaried employee:

James $80K salary; automatic withholding; overpaid $1,200 on taxes [$1200 refund].

Independent contractor:

Samantha freelance earnings of $50,000; pays Freelance Tax; estimated tax in 4 payments. Claims office supply and retirement expense deductions to reduce taxable income to $40,000.

There are different ways to reduce taxable income legally.

Business Owner:

Mark operates a small retail store, filing payroll returns & keeping track of operating expenses & paying Small Business Taxes quarterly. Through purchase depreciation and supplies he has reduced taxes due during the year by $6,000.

How Different Taxes Connect Together?

All types of taxes are related to one another. But it is vital to know federal vs. states tax and so on.

Federal income taxes are ultimately your biggest liability.

There’s also state income tax explained which varies from state to state, capital gains tax from your investments versus salary tax from earning an income.

Knowing how taxes are related will help you avoid double counting and/or overpaying.

Many different types of taxpayers will benefit from knowing how all of these taxes interact together. Below we will explain a few different examples:

Example Table – Interconnected Tax Example:

| Tax Type | Amount | Notes |

| Federal Income Tax | $6,500 | Based on taxable income $55,000 |

| State Income Tax | $3,200 | California resident |

| Payroll Tax | $5,000 | Social Security + Medicare |

| Capital Gains Tax | $1,000 | Sold stocks with profit $10,000 |

Real-Life Tax Scenarios

Retiree Scenario

Margaret retired last year with $60,000 in pension income and $10,000 in investment dividends.

Most of her pension income is subject to federal income tax and her investment dividends will be subject to capital gains tax.

Margaret used the tax deduction for medical expenses and received a standard deduction for being married, which allowed to reduce her taxable income by $12,000 when filing.

She also received a Retirement Savings Contribution Credit, which reduced her tax amount owed by $500.

This is an example of how careful tax planning can reduce your tax liabilities even after you retire.

Gig Economy Worker

Alex works as a rideshare driver and food delivery person on a part-time basis; his total earnings from these jobs are about $40,000.

He owes self-employment tax on this income, which typically averages about 15.3% of all net income.

By tracking his daily business expenses (for example, mileage driven, phone usage, supply purchases), Alex is able to deduct those amounts from his taxable income.

Therefore, his final net taxable income will only equal about $32,000.

Lesson: Keeping detailed records can help avoid paying too much in taxes and can also assist in preparing for quarterly estimated tax payments.

Dual-Income Household

Lisa and Mark are both employed full-time and earn approximately $150,000 per year as a household.

As a result of filing jointly, they will qualify for a larger standard deduction on their income tax returns. But it is essential to know how to understand tax returns in the beginning.

The couple contributes to a 401(k) retirement plan and a health savings account (HSA). This decreases the couple’s taxable income to around $130,000.

They were also able to take advantage of tax credits available for having two qualifying children to lower their final income tax liability.

Insight: Filing as married and taking advantage of the larger standard deduction has the potential to save countless dollars each year when compared to filing singly.

Tax Optimization Strategies

To make tax planning actionable, let’s dive deeper into numbers.

| Strategy | Who It Helps | Example Calculations | Notes |

| 401(K) Contribution | Salaried Employees | John gives $10,000 of his $80,000 salary | $2,200-$3,000 depending on tax bracket |

| Home Office Deduction | Freelancers | Sarah takes $1,500 for utilities and business expenses | $1,500 less taxable income |

| Child Tax Credit | Families With Dependents | Lisa and Mark have 2 children | $4,000 reduces taxes owed directly |

| Education Credits | Students/Parents | Alex pays $5,000 for school | $1,500 credit applied to tax owed |

| Health Savings Account | Any with High-Deductible Plan | Contributed $3,850 | Reduces AGI, reduces taxes by $800 to $1,000 |

Step-by-Step Example – Freelancer Optimization:

- Gross Income $50000

- Home Office deduction -$1500

- Remaining $48500

- Equipment Expense Deduction -$500

- Remaining $48000

- HSA Contribution (Health Savings Accounts) -$3850

- Remaining $44150

- Taxable Income $44150

- Reduce federal taxes by approximately $4500

This demonstrates how proper planning can make a significant difference.

Step-by-Step Filing Guide for Small Business Owners

Small businesses have many complex filings, so here’s a straightforward way to go about it:

1. Use accounting software to track all income and expenses.

2. Keep personal and business banking separate to reduce errors.

3. Use last year’s profit to establish estimated quarterly taxes due.

4. Keep track of your deductions such as:

- Rent for office space

- Direct costs related to your business

- Employee wages

- Depreciation

5. Submit the required forms (Schedule C, Form 1040, payroll tax returns) and make all payments on time to avoid penalties.

Example Table – Small Business Filing:

| Steps | Form/Action | Examples |

| Income Reporting | Schedule C | $120,000 gross revenue |

| Deduction | Business Supplies | $15,000 |

| Payroll | Form 941 | $20,000 paid to workers |

| Estimated Tax | Form 1040-ES | $10,000 quarterly payments |

By adhering to these guidelines, individuals like Tom will not only bypass burdensome audits but also conserve many thousands of dollars.

How Different Taxes Connect?

No tax exists in a vacuum. Proper knowledge of their interrelationships leads to proper tax planning:

- Federal Tax /State Tax – By filing jointly, taxpayers can maximize the use of deductions and credits available at both the federal and state tax levels to arrive at the amount of their total taxes owed.

- Payroll Tax / Self Employment Tax– Most freelancers pay both types of these taxes; also, both types have deductions that reduce taxable income.

- Capital Gains Tax – A capital gains tax is only assessed on investment gains. However long-term investment gains qualify for a reduced tax rate compared to short-term.

- Sales/Property Taxes – Though these types of taxes have no direct link to federal taxes, you must include these taxes when creating an overall financial plan.

Example – Combined Tax Snapshot:

| Tax Type | Amount | Notes |

| Federal Income Tax | $6500 | Based on taxable income $55,000 |

| State Income Tax | $3200 | California resident |

| Payroll Tax | $5000 | Social Security + Medicare |

| Capital Gains Tax | $1000 | Sold stocks with profit $10,000 |

| Property Tax | $6000 | Homeowner in NYC |

This table shows how multiple taxes add up and why planning across all types is crucial.

Final Thoughts

Understanding the U.S. tax system may seem intimidating, but by taking it one step at a time (e.g., from earning money all the way to filing your return), you will find it more manageable.

Effective planning, proper record-keeping, and utilizing the allowances and credits available to you under the law will allow for a reduction in your tax liability while remaining compliant with the law.

Taxes are not merely a legal obligation; taxes are another way of managing your finances and planning for your future.

Take Charge of Your Taxes

It is important to begin tracking your income, maintain proper records, and plan for allowable deductions early in the year.

In addition, utilize calculators to estimate your take-home pay and consider what methods you can use to legally reduce your tax liability.

By taking these steps, you can minimize the stress of filing your taxes and keep more of your money that you’ve worked very hard to earn.

FAQS

1. What is a tax system and how does it work?

A tax system is a way a government collects money from people and companies to pay for the things that the government provides (public services). Taxes are collected based on how much income, money spent, or value of property you have. This money is then used to help pay for certain things such as roads, schools, or the military.

2. How to calculate tax step by step?

Step 1: Find your total (gross income).

Step 2: Take out deductions (everything that you can take off your taxes).

Step 3: Calculate your taxable income.

Step 4: Multiply your taxable income by the current tax rate.

Step 5: Subtract any tax credits.

Step 6: Add in any other taxes (Self-Employment Tax, for instance).

After you’ve completed these steps, you should know either the total amount you owe the government, or if you have overpaid taxes, the amount of your refund.

3. Why do tax brackets exist?

Tax brackets allow for taxation to be done on a progressive basis, meaning that the higher the income, the higher the tax rate someone pays. This creates a fair way to distribute the overall tax burden by the total level of income.

4. What is taxable income vs gross income?

The term gross income is used to describe all forms of income that you have earned (ex: wages, commissions, bonuses, interest). Taxable income is the gross income you make from all sources, minus your deductions and exemptions, which will be used to determine the total amount of taxes you owe.

5. How do tax credits reduce tax liability?

Tax credits directly reduce a taxpayer’s tax liability on a dollar for dollar basis. Thus, if you are entitled to a $1,000 tax credit your tax bill will be reduced by $1,000. Some tax credits are also refundable meaning that if your credit exceeds the total of your tax liability, you will receive a refund.

6. When should you file taxes in the USA?

Tax Returns are generally due on April 15 of each year. If April 15 falls on a Saturday or Sunday or any other holiday, then the due date for the tax return will be extended. Taxpayers may also apply for an extension of time to file; however, they still must pay any taxes owed by the original due date.

7. What happens if you don’t file taxes?

Failing to file taxes can result in penalties, interest charges and/or legal action. The IRS will also file a return for you which may also be at an amount higher than what you would have submitted had you filed your return yourself.

8. How to legally reduce taxes?

Make claims for deductions (mortgage interest paid, medical expenses paid out-of-pocket, student loan interest paid).

Take advantage of credits available (child care credits, energy efficiency credits, education credits).

Make contributions toward a retirement account (i.e. 401.K, IRA).

Utilize Tax Efficient Investments.

All above are approved by the IRS rules as valid methods to reduce your tax liability (i.e. taxable income or amount of taxes owed).

9. What is AGI and why is it important?

Adjusted Gross Income (AGI) = Total of all earned income (less certain adjustments: contributions to retirement accounts) = how you determine whether you qualify for deductions or credits and what tax bracket you fall within.

10. How does filing status affect taxes?

Your filing status (i.e., Single / Married Filing Jointly / Head of Household) will determine how to calculate your tax obligation, your choice of your standard deduction, and your eligibility to claim certain credits). For example, Most married taxpayers receive a lower tax burden when filing their returns as a couple than when they file their returns separat