If you’ve ever looked at your paycheck and wondered where a chunk of your earnings goes, you’re not alone. Federal income tax USA rules can feel confusing at first, especially when you hear terms like “tax brackets,” “marginal rate,” or “taxable income.”

But once you break it down step by step, it starts to make sense. The system is actually structured in a logical way, designed to tax people fairly based on how much they earn. In this guide, we’ll go deep into how federal income tax brackets, federal income tax rates, and the overall system work, without the jargon overload.

What Is Federal Income Tax?

Definition and Purpose

Federal income tax in the USA is a tax collected by the IRS on income earned by individuals, businesses, and other entities. It’s one of the main sources of funding for the federal government and supports programs like infrastructure, defense, education, and public services.

In simple terms, it’s a percentage of your income that you pay to the government based on how much you earn.

Who Must Pay Federal Income Tax?

Most people who earn income in the United States are required to pay federal income tax, including:

- Employees receiving wages (W-2 workers)

- Self-employed individuals and freelancers

- Business owners

- Investors earning dividends or capital gains

However, not everyone is required to file, depending on income level, filing status, and age.

Sources of Taxable Income

Not all money you receive is treated the same. The IRS taxes many types of income, including:

- Wages and salaries

- Freelance or contract income

- Rental income

- Investment income

- Business profits

Understanding what is considered taxable is key to accurately calculating taxable income.

Role of the IRS

The IRS tax system is responsible for:

- Setting federal tax brackets

- Collecting taxes

- Issuing refunds

- Enforcing compliance

- Providing IRS tax tables explained for taxpayers

Overview of the US Tax System

The United States uses a progressive tax system, meaning:

The more you earn, the higher your tax rate on additional income.

But importantly, not all your income is taxed at the highest rate, only portions of it.

Federal Income Tax Brackets Explained

What Tax Brackets Mean?

Federal income tax brackets explained for beginners are simple:

A tax bracket is a range of income that is taxed at a specific rate.

For example:

- Income up to a certain amount → lower tax rate

- Higher income portions → higher tax rate

You don’t pay one flat rate on everything you earn.

Progressive Tax System Explanation

In a progressive taxation system:

- Low income is taxed lightly

- The middle income is taxed moderately

- High income is taxed at higher rates

But only the income within each bracket is taxed at that bracket’s rate.

Marginal vs Effective Tax Rate

This is where most confusion happens.

| Term | Meaning |

| Marginal tax rate | Tax rate on your next dollar earned |

| Effective tax rate | Your overall average tax rate |

For example:

- You might be in the 22% bracket

- But your effective tax rate might be 14%

This difference is critical in understanding your real tax burden.

Current Tax Bracket Ranges (Simplified Example)

| Income Range | Tax Rate |

| Low income | 10% |

| Middle income | 12% – 22% |

| Higher income | 24% – 37% |

These are simplified ranges based on the IRS tax brackets explained structure.

Example of Bracket Application

Let’s say you earn $60,000.

You don’t pay one rate on all $60,000. Instead:

- First portion taxed at 10%

- Next portion at 12%

- Remaining at 22%

This is how federal income tax brackets work in practice.

How Federal Income Tax Is Calculated?

Step 1: Determining Gross Income

Gross income includes everything you earn before deductions:

- Salary

- Business income

- Side income

- Investments

Step 2: Calculating Adjusted Gross Income (AGI)

Adjusted Gross Income (AGI) is your income after certain adjustments, such as:

- Retirement contributions

- Student loan interest

- Health savings accounts

AGI is a key figure used by the IRS.

Step 3: Subtracting Deductions

You can choose:

- Standard deduction

- Itemized deductions

This reduces your taxable income.

Step 4: Determining Taxable Income

After deductions:

Taxable Income = AGI – Deductions

This is what your tax brackets apply to.

Step 5: Applying Tax Brackets

Once taxable income is determined, it is taxed using federal tax rates for individuals explained through progressive brackets.

Example Federal Tax Calculation

Here’s a simplified federal income tax example calculation:

| Step | Amount |

| Gross income | $70,000 |

| Adjustments | -$5,000 |

| AGI | $65,000 |

| Deductions | -$14,000 |

| Taxable income | $51,000 |

That $51,000 is what gets taxed across brackets.

Filing Federal Income Taxes

Filing your taxes is a core part of the federal tax system, and once you understand the structure, it becomes far less intimidating. The key is knowing who must file, when deadlines apply, which forms are needed, and how modern tools simplify the process. Let’s break it down clearly with practical tables and examples so you can connect everything to real-world filing.

Who Must File a Federal Tax Return?

You are required to file a federal tax return if you meet certain conditions set under the federal tax filing rules in the USA. These rules ensure all taxable income is properly reported and included in your tax liability calculation.

Filing Requirement Overview

| Situation | Must File? | Explanation |

| Income above IRS minimum threshold | Yes | Standard requirement based on filing status |

| Self-employment income | Yes | Includes freelance, contractor, gig work income |

| Investment income (taxable) | Yes | Dividends, capital gains, interest income |

| No taxable income | Usually no | Unless taxes were withheld and refund is due |

Even if you are below the threshold, filing may still be beneficial to claim refunds or credits.

IRS Filing Deadlines

Deadlines are a critical part of federal income tax USA compliance. Missing them can increase your tax costs due to penalties and interest.

Key Filing Dates

| Event | Date | Notes |

| Standard tax filing deadline | April 15 | Applies to most taxpayers |

| Filing extension deadline | October 15 | Extra time to file, not to pay |

| Estimated tax payments | Quarterly | For self-employed individuals |

It’s important to understand:

Extensions only delay filing paperwork, not your tax payment obligation.

This directly impacts your final tax liability calculation, especially if payments are delayed.

Filing Statuses Explained

Your filing status determines how your income is taxed under federal income tax brackets and affects your deductions and credits.

Filing Status Comparison

| Filing Status | Who Uses It | Tax Impact |

| Single | Unmarried individuals | Standard brackets, fewer benefits |

| Married Filing Jointly | Married couples | Usually, a lower overall tax rate |

| Head of Household | Single with dependents | Lower tax rates + higher deductions |

Your filing status directly influences your taxable income calculation and placement within the IRS tax brackets.

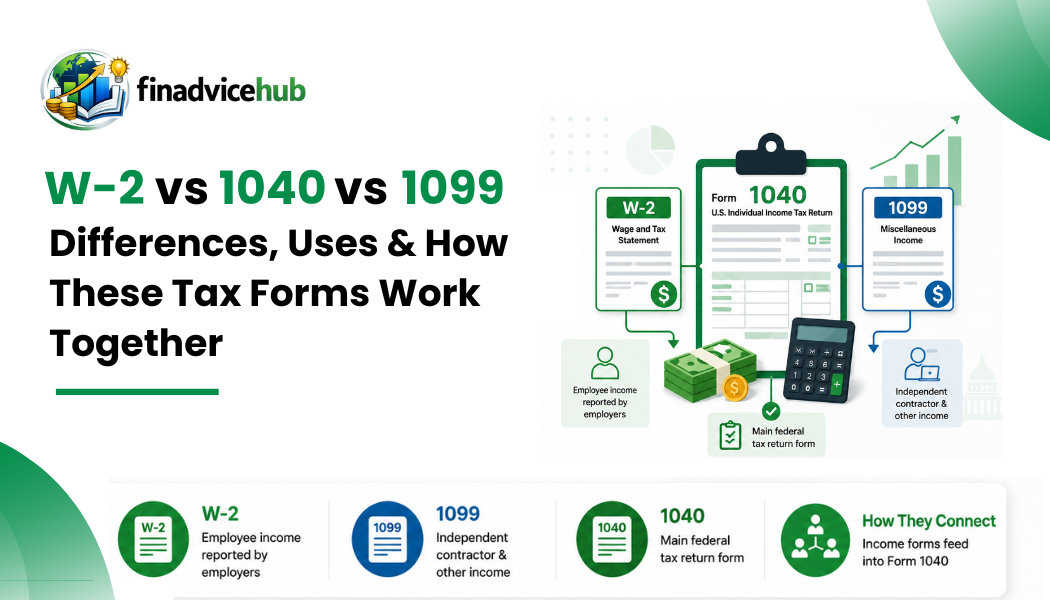

Required IRS Forms

Different income sources require different IRS forms. These documents feed into your final federal income tax calculation.

Common Tax Forms

| Form | Purpose | Who Uses It |

| Form 1040 | Main tax return form | All taxpayers |

| W-2 | Wage reporting | Employees |

| 1099 | Freelance/contract income | Independent contractors |

| Schedule C | Business income/expenses | Self-employed individuals |

| Schedule SE | Self-employment tax calculation | Freelancers & contractors |

Each form contributes to determining your final tax liability calculation and ensures accurate reporting under the federal tax system.

Online Tax Filing Process

Modern tax filing has become significantly easier due to digital tools, automation, and AI-based systems. These tools help taxpayers understand how federal income tax works and estimate their obligations before filing.

Digital Tax Filing Tools

| Tool Type | Function | Benefit |

| IRS e-file system | Direct online filing | Faster processing & refunds |

| Federal income tax calculator | Estimates tax owed | Helps with planning |

| Tax bracket calculator USA | Shows bracket placement | Improves tax understanding |

| AI tax planning software | Automated tax insights | Suggests deductions & optimizations |

| Automated tax estimation tools | Real-time tax tracking | Reduces surprises at filing time |

These tools help you:

- Estimate your taxable income calculation before filing

- Understand your position in federal income tax brackets

- Improve accuracy in tax liability calculation

- Avoid mistakes in reporting income

Simplified Filing Flow

To connect everything, here’s how the process typically works:

Step-by-Step Filing Overview

| Step | Action | Outcome |

| 1 | Gather income documents (W-2, 1099) | Total income identified |

| 2 | Calculate adjusted gross income (AGI) | Income adjustments applied |

| 3 | Apply deductions | Taxable income reduced |

| 4 | Apply tax brackets | Final tax calculated |

| 5 | File via IRS e-file | Return submitted |

This structured process ensures your federal income tax calculation is accurate and aligned with IRS rules.

Factors That Affect Federal Tax Liability

Your total federal income tax bill in the USA isn’t determined by one simple number. Instead, it depends on several moving parts that work together, your filing status, income sources, deductions, credits, and even how well you plan. Understanding these factors helps you make smarter decisions throughout the year instead of reacting at tax time.

Filing Status

Your filing status is one of the most powerful factors in determining your tax liability calculation. It directly affects your federal income tax brackets, standard deduction amount, and overall tax rates.

The IRS uses filing status to decide how your income is taxed under the progressive tax system in the USA, meaning two people earning the same income can pay very different taxes depending on their status.

Common Filing Statuses and Impact

| Filing Status | Who It Applies To | Tax Impact |

| Single | Unmarried individuals | Standard brackets, higher rates compared to some others |

| Married Filing Jointly | Married couples combining income | Usually, a lower effective tax rate |

| Married Filing Separately | Married couples filing separately | Often, a higher tax burden overall |

| Head of Household | Single with dependents | Lower rates + higher deductions |

Choosing the correct status is essential because it directly affects your taxable income calculation and determines which IRS tax brackets explained structure applies to you.

Income Type

Not all income is taxed the same way. One of the most important parts of understanding how federal income tax works is recognizing how different income streams are treated under the federal tax system.

Types of Taxable Income

| Income Type | How It’s Taxed | Key Notes |

| Salary/Wages | Standard federal tax rates | Withheld automatically from paycheck |

| Investment Income | Capital gains rates | Often lower than regular income tax rates |

| Freelance Income | Ordinary income tax rates + self-employment tax | Requires self-reporting and Schedule SE |

For example, a freelancer earning $60,000 may face both federal tax rates for individuals explained plus additional self-employment taxes, while an investor may benefit from lower capital gains rates.

Understanding what income is taxable federally helps you avoid surprises and improves your tax planning strategies.

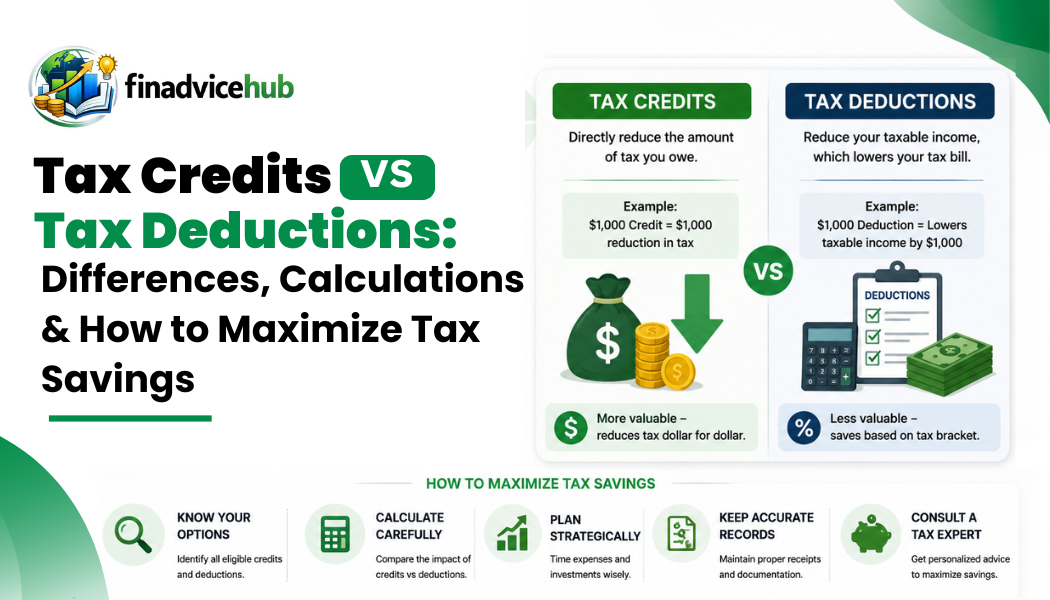

Deductions and Credits

Deductions and credits both reduce your taxes, but they work in different ways, and this difference is often misunderstood.

- Deductions reduce your taxable income

- Credits reduce your actual tax owed

This directly impacts your taxable income calculation and final tax liability calculation.

Deductions vs Credits Comparison

| Type | How It Works | Example Impact |

| Deduction | Lowers taxable income | Reduces income before tax brackets apply |

| Credit | Reduces tax directly | Lowers the final tax bill dollar-for-dollar |

For example:

- A $1,000 deduction might save you $120–$240, depending on your bracket

- A $1,000 credit saves you exactly $1,000 in tax

This is why understanding deductions is a key part of federal tax filing rules in the USA and effective tax planning.

Dependents

Having dependents, such as children or qualifying relatives, can significantly reduce your tax burden through credits and deductions.

Dependents affect your taxes in multiple ways:

- Higher standard deduction in certain filing statuses

- Eligibility for child tax credits

- Additional dependent care credits

This directly lowers your overall tax liability calculation, especially for households qualifying under Head of Household status.

In simple terms, dependents can shift you into a more favorable tax position within the federal income tax brackets system.

Tax Planning Strategies

Smart tax planning helps you legally reduce your taxes instead of reacting at the end of the year. Many people underestimate how much control they actually have over their federal income tax calculation.

Here are some widely used strategies:

Common Tax Planning Approaches

| Strategy | How It Helps |

| Retirement contributions | Lowers taxable income while building savings |

| Timing income | Shifting income between tax years to stay in lower brackets |

| Maximizing deductions | Reduces overall taxable income |

| Using tax credits | Directly reduces tax owed |

These strategies are especially useful when combined with tools like a federal income tax calculator, tax bracket calculator USA, or modern AI tax planning software, which can help estimate outcomes in real time.

For example:

- Contributing to a retirement account can reduce your taxable income and potentially keep you in a lower federal income tax bracket

- Deferring income might help you avoid moving into a higher marginal tax rate in a given year

Common Federal Tax Mistakes

Even when people understand the basics of federal income tax in the USA, mistakes still happen, and often they’re not small ones. The IRS system is detailed, and even a simple misunderstanding can increase your tax bill or trigger penalties. Let’s break down the most common errors in a practical, easy-to-understand way so you can avoid them.

Misunderstanding Tax Brackets

One of the biggest misconceptions about federal income tax brackets is the belief that earning more money pushes all of your income into a higher tax rate. This is not how the system works.

The U.S. uses a progressive tax system, which means only portions of your income are taxed at different rates. This is tied to the concept of a marginal tax rate, not a flat tax on everything you earn.

For example, if you move into a higher tax bracket:

- Only the income above the previous bracket is taxed at the higher rate

- The lower portions of your income remain taxed at lower rates

So if you hear someone say, “I don’t want to earn more because I’ll jump into a higher tax bracket,” that’s a misunderstanding. Earning more may increase your taxes slightly, but it never reduces your overall income due to a higher bracket.

Understanding this difference between marginal and effective tax rate, explained clearly, helps you make smarter financial decisions without unnecessary fear of earning more.

Incorrect Filing Status

Your filing status plays a major role in determining your taxable income calculation, your deductions, and your overall tax liability. Choosing the wrong one is a surprisingly common mistake.

Filing statuses include:

- Single

- Married Filing Jointly

- Married Filing Separately

- Head of Household

Each status has different tax brackets and deduction limits. For example, the Head of Household generally offers lower tax rates and higher standard deductions compared to filing as “Single,” but you must qualify properly.

A common issue occurs when taxpayers:

- Choose “Single” even though they qualify for Head of Household

- Filing jointly when separating finances would be more beneficial in rare cases

- Don’t update their status after marriage or divorce

This mistake can quietly increase your tax liability calculation without you realizing it. Using a tax bracket calculator, a USA or IRS tax estimator can help confirm the correct status before filing.

Missing Deductions

Failing to claim deductions is one of the easiest ways to overpay taxes. Deductions reduce your taxable income, which directly lowers how much you owe under the federal tax system.

Commonly missed deductions include:

- Student loan interest

- Retirement contributions

- Health savings account (HSA) contributions

- State and local taxes (SALT deduction, within limits)

- Self-employed business expenses

Many taxpayers either forget these or don’t keep proper records throughout the year. This leads to an inflated taxable income calculation, which then increases the total tax owed.

For example:

- If your income is $70,000

- And you miss $5,000 in deductions

- You’re effectively paying tax on income you didn’t actually keep

Using tools like a federal income tax calculator or automated tax estimation tools can help identify deductions you might be missing.

Underreporting Income

Underreporting income is one of the most serious mistakes in the federal tax filing rules in the USA. It can happen intentionally or accidentally, especially for freelancers and gig workers who receive multiple 1099 forms.

Common causes include:

- Forgetting side income (freelance gigs, digital platforms, cash work)

- Not tracking all 1099 forms

- Misreporting investment income

- Confusing gross vs net income

The IRS receives copies of most income reports directly from employers, banks, and financial platforms. This means mismatches are easy to detect.

Consequences can include:

- IRS notices requesting correction

- Interest on unpaid taxes

- Penalties for underreporting

- Increased audit risk

Even small errors matter because they affect your total tax liability calculation and can compound over time.

Filing Late

Filing your federal tax return late is another common mistake that can become expensive quickly. Even if you can’t pay your full tax bill, filing on time is still extremely important.

Late filing can result in two separate penalties:

- Failure-to-file penalty (higher and more serious)

- Failure-to-pay penalty (applies if taxes aren’t paid on time)

Interest also begins accruing on unpaid amounts, increasing your total cost over time.

Many people delay filing because:

- They are waiting for the missing documents

- They underestimate how long the federal tax filing rules in the USA actually take

- They assume penalties are small

In reality, delays can snowball into larger financial issues. Even if you’re unsure of your exact numbers, filing early with estimates and correcting later is often better than missing the deadline entirely.

Using an IRS tax estimator or federal tax withholding calculator can help you prepare in advance, so filing becomes smoother and less stressful.

Final Thoughts

Understanding federal income tax in the USA becomes much easier once you break it into steps: income, adjustments, deductions, and brackets. The system may seem complex at first, but it follows a clear structure based on the progressive tax system principles of the USA.

When you understand how federal income tax brackets, taxable income calculation, and marginal tax rate work together, you stop guessing and start planning. Instead of reacting at tax time, you can use tools like an IRS tax estimator or a federal tax withholding calculator to make smarter financial decisions throughout the year.

In the end, tax knowledge isn’t just about compliance; it’s about control, clarity, and making sure you keep more of what you earn.

FAQs

What is federal income tax?

It is a tax collected by the IRS on income earned by individuals and businesses.

How do federal tax brackets work?

They tax portions of income at different rates, not all income at one rate.

What is the difference between the marginal and the effective tax rate?

Marginal rate applies to your next dollar earned, while the effective rate is your average tax rate.

Who must file federal income tax returns?

Anyone earning above IRS thresholds or with taxable income sources.

How is taxable income calculated?

By subtracting deductions from adjusted gross income (AGI).

What income is not taxable federally?

Some benefits, like certain gifts, inheritances, and specific government benefits, may not be taxable.

How are federal tax rates determined?

They are set by Congress and updated periodically.

What happens if federal taxes are not filed?

You may face penalties, interest, and legal enforcement.